For five months, the tariff math on apparel has been unusually simple. That's about to change on a specific date.

After the Supreme Court struck down the administration's IEEPA “reciprocal” tariffs in February — a 6–3 ruling that emergency powers don't include the power to tax imports — the White House replaced them with a single flat surcharge. It applied to nearly everyone the same way.

That flatness is the thing about to end. And what replaces it turns your sourcing decision into a compliance decision — because your country choice now sets your tariff rate. Here's the new country-by-country stack, and the move before Fall POs lock.

The floor everyone got used to

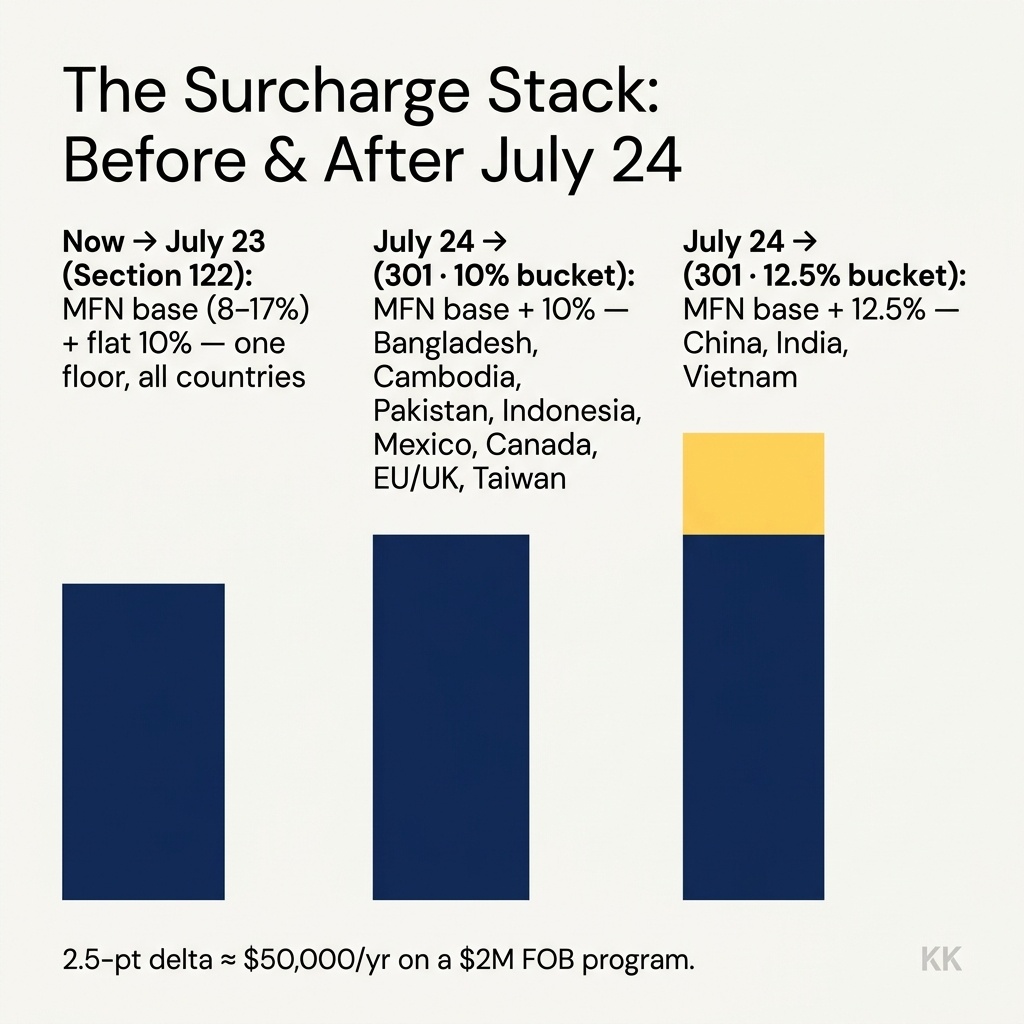

The surcharge on the way out is Section 122 (a balance-of-payments tool that lets the President impose up to 15% for a strictly limited window). It went live at a flat 10% on February 24, 2026, and it applied to nearly everyone alike (GHY International).

Vietnam, India, Bangladesh, Indonesia — the country you sourced from stopped changing your surcharge. The rate was a floor, and the floor was flat.

That uniformity is exactly what's about to break. Section 122's authority expires by its own terms on July 24, 2026, and it can't simply be renewed at will. When it goes, so does the one number that made your sourcing map look the same everywhere.

“The rate was a floor, and the floor was flat. That flatness is the thing about to end.”

Why July 24 is a real date, not a headline

Two forces make this a hard deadline rather than a maybe. First, the statute: Section 122 duties are capped at 150 days, and February 24 plus 150 days lands on July 24. There's no discretionary extension inside the law.

Second, the courts are pulling the same direction. In May, the Court of International Trade invalidated the Section 122 tariffs outright, though the ruling's practical effect is limited while it's appealed. The point for a founder isn't the litigation — it's that the 10% floor is living on borrowed time from two directions at once, and planning as if it's permanent is the mistake.

So the administration is building the replacement in the open. The vehicle is Section 301 (the same trade-law hook used for the China tariffs) — this time aimed at forced labor. USTR announced findings and proposed actions across 60 economies in June, with written comments due July 6 and hearings July 7. That timeline is why this lands on your desk now: the number your Fall program gets costed against is still being written.

The new map: 10% vs 12.5%

Here's the mechanic that changes sourcing from a cost question into a compliance one. USTR proposes two rates: 10% for economies that already ban forced-labor imports (or have committed to, or run a partial regime that blocks them), and 12.5% for everyone else. The dividing line isn't your cost sheet. It's the exporting country's own forced-labor enforcement policy.

And the two buckets cut straight through the apparel-sourcing world. The 10% group includes Bangladesh, Cambodia, Pakistan, Indonesia, Malaysia, Mexico, Canada, Guatemala, Taiwan, and the EU/UK — 14 economies in all. The 12.5% group is the remaining 46, and it includes China, India, and Vietnam — three of the four countries that make most of the world's clothes.

Read that against a real cost stack. Base MFN duty (most-favored-nation — the baseline rate WTO members' goods pay) on apparel already runs roughly 8% to 17% depending on fiber and construction — and layered surcharges pushed the average effective apparel duty to 35.1% by December 2025, up from 14.7% a year earlier. Against numbers that big, a flat 10% floor was noise. A 10%-vs-12.5% split is a lever — because now the surcharge moves with the country.

“The dividing line isn't your cost sheet. It's the exporting country's forced-labor policy.”

Signs the split will actually hit your margin

- • Your Fall program is single-sourced in a 12.5% country (China, India, or Vietnam) with no second origin costed.

- • Your customs value per unit is high enough that 2.5 points clears your per-unit margin cushion.

- • You've been quoting Fall landed costs off the flat 10% floor and haven't re-run them against the split.

Free download

The Fall Re-Cost Worksheet

A three-scenario landed-cost grid — 122-lapse, 301-at-10%, 301-at-12.5% — with the country-bucket list built in. Runs any FOB price across every outcome. PDF.

The textile mechanism nobody's pricing yet

There's a release valve buried in the proposal, and it's aimed directly at apparel. USTR floated a textile mechanism: a certain volume of apparel and textile imports from a given country could enter at a reduced Section 301 rate (USTR).

The volume isn't arbitrary. It's tied to how much that country buys from the US — specifically, the quantity of US textile exports it takes, plus the volume of US cotton and cotton products it imports. In other words, countries that buy American cotton earn a reduced-rate quota back on the apparel they ship in.

That's not final, and the mechanics — who administers the quota, how it's allocated — are exactly what the July 7 hearings exist to resolve. But it means the headline country rate isn't necessarily your rate. If your mill's country is a large US-cotton buyer, some of your volume may land under the reduced tier — worth asking your supplier before you assume the sticker rate.

The counter-case: why 2.5 points isn't the whole story

It would be easy to read this as “flee the 12.5% countries.” Don't — at least not on the tariff alone. The gap between India at 12.5% and Bangladesh at 10% is 2.5 points of customs value. On a $2M FOB Fall program that's about $50,000 a year — real, but small next to what a bad move can cost.

Because tariff is one line in a landed cost, and the rest of the lines don't move with it. Re-tooling a proven program into a new country to chase 2.5 points can hand back the savings in sampling rounds, quality drift, longer lead times, and MOQ resets — and the shelf date doesn't wait. A 12.5% origin with a mill that hits your quality and your calendar can still beat a 10% origin you've never run.

The honest read: the split is a reason to re-cost and diversify, not to panic-migrate. Know your number under each scenario, get a second origin costed so you have a lever — and treat the forced-labor rate as one input, not the verdict. That's the discipline behind a US-plus-one sourcing setup: a primary you trust, plus a costed alternate you can pull when the map moves.

The move before Fall POs lock

The window is open right now, and it closes on the calendar. Comments and hearings run July 6–7; the floor lifts July 24; Fall POs are landing in exactly that gap. Re-cost every open Fall program under three scenarios — 122 lapses to MFN only, 301 lands at 10%, 301 lands at 12.5% — so you're quoting a range, not a stale floor.

The flat floor made sourcing feel settled. It wasn't — it was just paused. If your Fall program is single-sourced in a 12.5% country and still quoted off the old 10% floor, the question isn't whether to worry; it's what your number is under each of the three outcomes. What we'd do in your shoes: re-cost this week, and get one alternate origin on paper before the POs lock.

Read next

8 min read

The July 24 Tariff Cliff

The deadline mechanics and the exact re-cost math for a Fall program.

8 min read

Every Parcel Pays Now: The End of the $800 Rule

What the end of duty-free small parcels means for DTC brands.

7 min read

The US-Plus-One Sourcing Playbook

Keep a primary origin and a costed alternate you can pull on demand.

Comments

No comments yet

Be the first to share your thoughts!