Every Fall purchase order you sign this month carries a number you can't actually see yet.

The landed cost — what the goods cost by the time they clear US customs — rides on a tariff regime with a hard expiration date stamped on it: July 24, 2026. That's 30 days out.

After it, the rulebook that's governed apparel duties since February could be gone, replaced, or stuck in court. So the PO becomes a wager — not on your factory, your fabric, or your delivery date, but on federal trade policy. Here's how to size that bet before you place it.

What expires July 24 — and what quietly doesn't

The thing sunsetting is the Section 122 surcharge (a provision of the Trade Act of 1974 that lets the President impose a temporary import duty of up to 15% for no more than 150 days to address a balance-of-payments problem) — a pressure valve, not a permanent tariff tool (Congressional Research Service).

The administration invoked it on February 24, 2026, at a flat 10% on nearly all imports, right after the Supreme Court ruled the earlier emergency tariffs unlawful (White & Case). The 150-day clock runs out July 24. The statute gives the President no unilateral extension — only an Act of Congress can lengthen it.

Two things do not expire with it, and both drive your math. The first is the MFN duty (most-favored-nation — the baseline rate every WTO member's goods pay regardless of trade fights), which on a cotton knit tee runs about 16.5% (2026 clothing-tariff guide). The second is China's Section 301 tariff (a separate 7.5% on apparel under List 4A, from the 2018–19 action) — different legal authority, no July sunset (Make Mine).

There's a live wrinkle, too. The US Court of International Trade struck down the Section 122 tariffs on May 7, 2026, calling the balance-of-payments justification unmet; the government has appealed to the Federal Circuit (Skadden). So the 10% could vanish by court order before July 24, or outlast it on appeal. Your PO bets on a calendar and a docket at the same time.

“The tariff everyone is watching is temporary. The one nobody mentions — about 16.5% on a cotton tee — isn't going anywhere.”

The spread didn't widen. It collapsed — for now

For most of 2025, sourcing country was a tariff decision. India carried an 18% reciprocal rate, Vietnam 46%, Bangladesh 37% — a real, country-by-country spread that pushed brands to chase the lowest line.

That spread is gone. When the flat 10% replaced the reciprocal schedule in February, India's rate dropped from 18% to 10%, and so did everyone else's (Tariffs Tool). India, Vietnam, Bangladesh, Cambodia — all sitting at the same blanket today.

“For thirty days, the cheapest country to import from and the most expensive are separated by a single line item only China still carries. That symmetry ends July 24.”

China is the exception, and only because its legacy 7.5% stacks on top of the same blanket everyone else pays. That's part of why Bangladesh just overtook China as the #2 apparel supplier to the US in early 2026 — $1.37B versus China's $1.17B in January–February, with Vietnam still #1 at $2.7B (The Business Standard). China's slide isn't the blanket. It's the 7.5% the blanket can't erase.

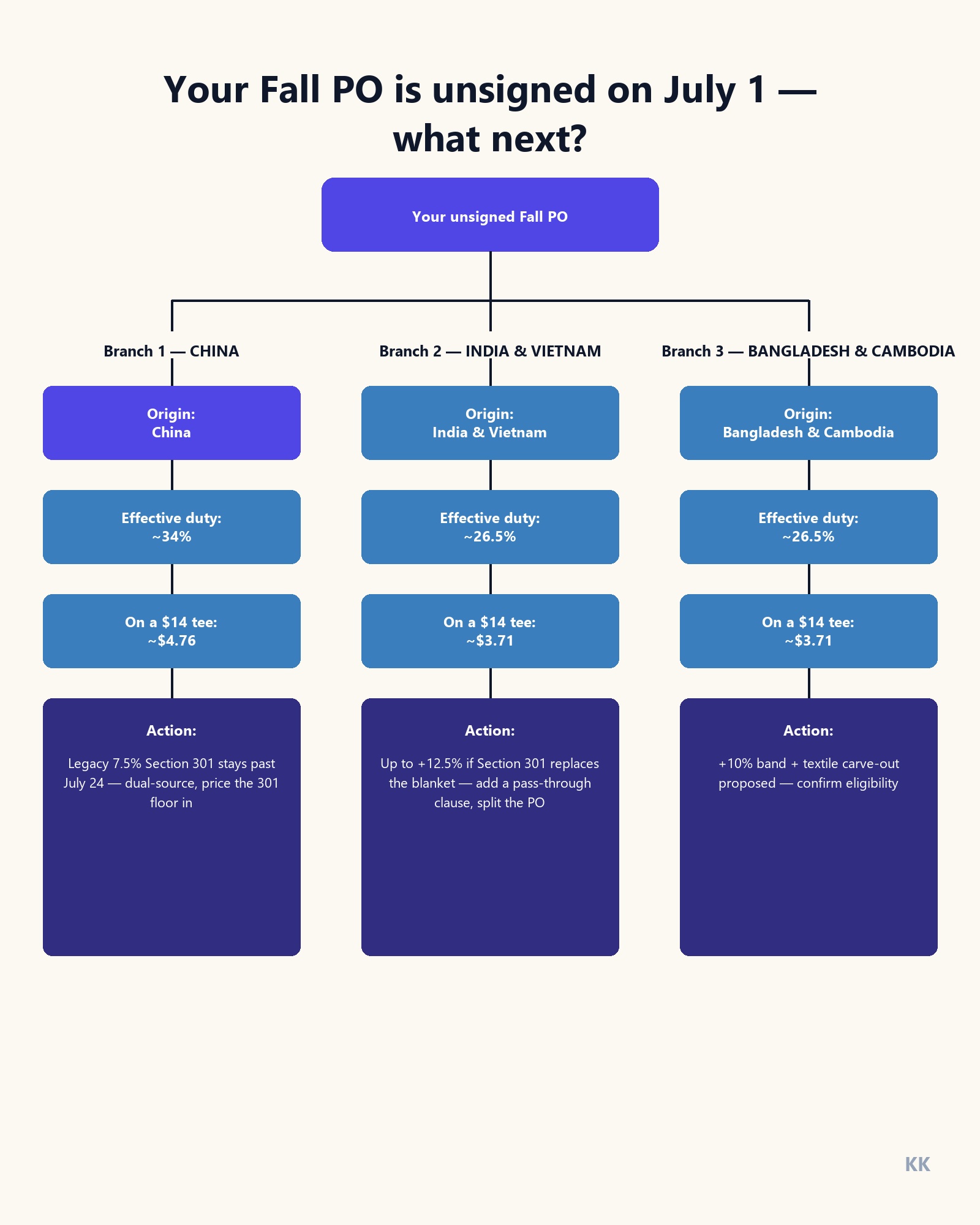

The $14 tee, three ways

Put a real garment through it. A blank cotton knit tee at $14 FOB (free on board — the supplier's price at the origin port, before freight and duty). Duty is assessed on that customs value.

Today, before the cliff:

- India: 16.5% MFN + 10% Section 122 = $3.71/tee (26.5%)

- Vietnam: same stack = $3.71/tee (26.5%)

- Bangladesh: same stack = $3.71/tee (26.5%)

- China: 16.5% + 10% + 7.5% Section 301 = $4.76/tee (34%)

The only live gap is China's extra $1.05 a tee — about $5,250 on a 5,000-unit run. Every other origin is a tie.

After July 24, the bet has a range, not a number:

- If the blanket lapses and nothing lands in time, duty drops to MFN alone — $2.31/tee (16.5%). You'd be over-costed today.

- If the pending Section 301 duties replace it, the proposal is +10% for Bangladesh and Cambodia and +12.5% for India and Vietnam (White & Case). That puts India near $4.06/tee (29%) — and a separate excess-capacity docket covering 16 economies could stack more on top (White & Case).

So the duty on that same tee lands somewhere between $2.31 and $4.06-plus. A $1.75 swing per unit you can't price yet — roughly $8,750 of unknown on a 5,000-piece Fall buy.

Free download

The Fall 2026 Tariff Re-Costing Worksheet

A one-page model that runs any FOB price across all four origins at today's rate and every post-July scenario, with the pass-through clause language built in. PDF.

Re-costing Fall without re-opening every PO

You don't need to predict the outcome. You need POs that survive every branch of it.

“Price the landed cost, not the FOB. The FOB is the only number on your PO that won't move this summer.”

Three moves do most of the work. Split the PO across two origins so one ruling can't reprice your whole Fall buy — a China-plus-Bangladesh split hedges the 7.5% that won't sunset against the blanket that might. Write a tariff pass-through clause that defines who absorbs duty changes between order and delivery, so a July ruling doesn't become a renegotiation. And build a contingency line into landed cost at the high end of the range, not the current rate — if duties fall, that's margin recovered, not a hole.

One nuance worth knowing: the Section 301 proposal includes a textile mechanism that would let a set volume of apparel from certain countries enter at a reduced rate (USTR). If your origin qualifies, your post-July number could be lower than the headline rate. Confirm eligibility before you assume the worst case.

Signs your Fall PO is exposed to the cliff

- • The cost sheet quotes FOB, with duty as a footnote or "TBD."

- • Your entire Fall buy sits in one country of origin.

- • There's no clause naming who eats a mid-shipment duty change.

- • You're costed at today's 10%, with no contingency if it's replaced higher.

The case for not moving a thing

Re-costing isn't the same as re-sourcing, and the second one can cost more than the tariff it's chasing. If you're already on India, Vietnam, or Bangladesh, you're at the blanket rate — there's no cheaper origin to flee to right now, because the spread collapsed.

Remember which number actually dominates: the 16.5% MFN duty is the largest, most permanent slice of that tee, and it doesn't care who wins in court. Chasing a 2.5% country delta by switching factories 30 days before Fall can blow your delivery window — and the shelf goes to a competitor who shipped.

Sometimes the right move is a sharper contract, not a new passport on your goods.

What we'd do in your shoes

We'd cost every open Fall PO twice — at today's 10% and at the high end of the post-July range — and sign nothing whose margin only works at the lower one. We'd split origin where the volume allows it, and put a tariff pass-through clause in every contract before the 24th.

The blanket made every sourcing decision look equal for a few months, and that quiet is about to break. If you had to sign a Fall buy this week, which line on the cost sheet would you defend first?

Read next

7 min read

Why US Fashion Brands Are Moving Production From China

The 7.5% that won't sunset — and what it means for your next run.

9 min read

The 'Made in India' Trend Reshaping American Luxury

Why the 10% line made India the quiet winner of 2026.

7 min read

What to Lock for Holiday Before the Window Closes

Tariffs aren't your only clock. The calendar is closing too.

Comments

No comments yet

Be the first to share your thoughts!